Despite its impressive performance in 2020 and 2021, it’s no secret that Pfizer (NYSE: PFE) is in the process of reinventing itself. Without much of the windfall from its coronavirus products propping up the top line, it may be years until revenue can top its recent peak.

But that just means the company has an incentive to make big plays and take big risks to delight its shareholders. On that front, here’s my prediction for what its next major move will be.

There’s a big incentive to acquire a certain kind of biotech right now

At the moment, Pfizer’s grand plan is to lay the groundwork for its growth through 2030 and beyond. As part of that plan, it expects to add $20 billion in revenue from sales of new medicines produced with its own research and development (R&D) capabilities, and $25 billion from acquisitions of other biopharmas and their most promising pharmaceutical assets.

When it recently bought Seagen, a cancer biotech with advanced therapeutic technology, it was willing to take on $31 billion of debt to make the purchase. Cancer will remain one of Pfizer’s new major focuses, per management. But there’s another area that it’s eyeing where it hasn’t made a similarly big move: weight loss.

Though medicines made by Eli Lilly and Novo Nordisk have been wildly successful, Pfizer’s own weight loss programs haven’t exactly worked out as intended. Some candidates have been canceled entirely, and its most advanced programs are still in phase 1 clinical trials — many years away from being commercialized, assuming they ever are. With a market that could be worth as much as $130 billion by 2030 on the line, slogging ahead, then entering long after the current contenders have had years to secure market share, simply won’t do.

Therefore, my prediction is that Pfizer’s next big move will be to acquire a promising biotech with late-stage weight loss programs, or to acquire such programs directly and finish the development process in-house. Here’s why this move is a real possibility.

First, the company has plenty of money. As of the first quarter, it has more than $11.9 billion in cash, cash equivalents, and short-term investments on hand. It also has just over $68.7 billion in debt, giving it a debt-to-equity ratio of 0.7. In other words, it has a lot of money on hand, and while it’s starting to look a bit indebted, it probably still has more than enough flexibility to borrow significant volumes of cash if necessary.

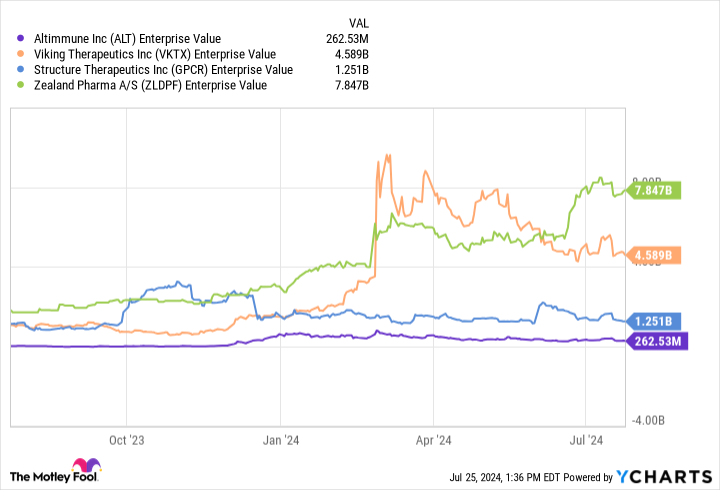

Pfizer is so well-capitalized, in fact, that it could afford to buy more than one of the leading biotechs developing anti-obesity medicines. Check out this chart describing the enterprise value (EV) of players like Viking Therapeutics, Altimmune, Structure Therapeutics, and Zealand Pharma:

The actual acquisition price of these businesses might be higher than their EVs imply. But they’re well within what Pfizer can afford today — assuming it’s a faster entry into the market for weight loss drugs that the company is aiming to do.

However, buying these biotechs entirely, or buying their lead assets, might not even be necessary for Pfizer to get the exposure it wants. It could easily opt to forge a development collaboration instead, taking on a smaller cost burden in exchange for a lower ceiling on possible earnings from future sales. If anything, it’s surprising that Pfizer hasn’t done more collaborations on the weight loss front already.

Don’t count the eggs until they hatch

It’s probable that Pfizer’s stock would see a significant bump on the day it were to announce an acquisition of a weight loss biotech, assuming this prediction comes true.

But until that day comes, don’t buy this stock with the expectation that an announcement is right around the corner. Likewise, recognize that sometimes clinical trials fail, even in the late-stage programs that are the juiciest targets for purchasing. There’s a risk that an acquisition could end with little to show for the expenditure.

In addition, consider that it could be a better move to invest in one of these biotechs than in Pfizer itself at the moment. If the bigger business makes a bid to buy it, you’ll benefit that way too.

Should you invest $1,000 in Pfizer right now?

Before you buy stock in Pfizer, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Pfizer wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $692,784!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of July 22, 2024

Alex Carchidi has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Pfizer. The Motley Fool recommends Novo Nordisk. The Motley Fool has a disclosure policy.

Prediction: This Will Be Pfizer’s Next Big Move was originally published by The Motley Fool