[ad_1]

Share prices of Palantir Technologies (NYSE: PLTR) fell more than 6% after the high-flying software platforms provider received an analyst downgrade. Analyst Brian White of brokerage Monness, Crespi, Hardt & Co. downgraded the stock to sell from neutral, predicting that it could get a reality check following its impressive surge in the past year.

Palantir stock has rocketed 185% in the past year thanks to the company’s growing credentials in the artificial intelligence (AI) software market. White’s price target of $20 suggests that Palantir could drop 13% from current levels because of its rich valuation. Is this a warning for investors to hit the sell button, or should savvy investors consider Palantir’s latest pullback as a buying opportunity? Let’s find out.

Palantir Technologies is indeed expensive right now

White points out that the “unprecedented generative AI hype cycle” has brought Palantir stock to “an egregiously rich valuation.” A closer look at the company’s multiples indicates the analyst isn’t wrong.

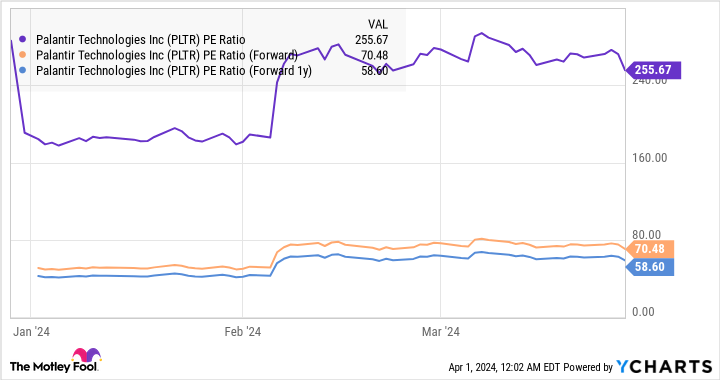

Palantir now commands a price-to-sales ratio of 24.6. Additionally, it is trading at a whopping 264 times trailing earnings. Those multiples are substantially higher than the Nasdaq-100 Technology Sector index’s sales multiple of 7.3 and earnings multiple of 47.

It is also worth noting that Palantir’s growth has not been as solid as some other AI stocks. The company’s 2023 revenue was up only 17% from the previous year. However, full-year earnings quadrupled year over year to $0.25 per share last year from $0.06 per share in 2022, driven by a robust improvement in the company’s margin profile.

Palantir’s CEO, Alex Karp, pointed out on the company’s February earnings conference call that the company enjoys “strong unit economics,” which simply means that it is making more money from each customer that it acquires. So, while Palantir’s top-line growth may not be really solid right now to justify its sales multiple, its earnings growth is quite impressive.

More importantly, consensus estimates indicate that Palantir could maintain its outstanding earnings growth over the long run, clocking an annual earnings growth rate of 85% for the next five years. If Palantir can indeed maintain that pace, it may be able to justify its rich valuation. For instance, applying the projected earnings growth rate of 85% for the next five years to Palantir’s 2023 earnings indicates that its bottom line could increase to $5.42 per share at the end of 2028.

The Nasdaq-100 has an average forward earnings multiple of 28. Assuming Palantir trades at a similar multiple after five years and achieves the projected earnings calculated above, its stock price could jump to $150 per share. That would be a huge jump from current levels. This impressive growth that analysts are expecting Palantir to deliver explains why its forward earnings multiples are much lower.

So, the only way Palantir stock could sustain its red-hot rally is by maintaining a high pace of earnings growth. And for that to happen, its revenue growth will have to accelerate as well. The good part is that the company’s recent quarterly results indicate that it could indeed see faster revenue growth thanks to AI.

AI is accelerating Palantir’s business

For Palantir, AI is more than just hype. That’s because the proliferation of this technology is indeed driving tangible growth for the company. This is evident in a few simple metrics.

In the fourth quarter of 2023, Palantir closed 103 deals that were worth at least $1 million. That was a big jump over the 55 deals worth at least $1 million it closed in the same period last year. Even better, customers are now signing bigger deals with Palantir. It reported 37 deals worth at least $5 million in the fourth quarter of 2023, along with 21 deals worth $10 million or more. That was a big jump over the year-ago period’s count of 11 deals worth $5 million or more and five deals worth at least $10 million.

This stronger deal activity explains why Palantir ended 2023 with $1.24 billion in remaining performance obligations (RPO), up nearly 28% from the year-ago period. The metric refers to the total value of a company’s future contractual obligations, so the fact that it grew at a faster pace than Palantir’s top line indicates that the company is setting itself up for robust long-term growth.

Palantir credits the growing adoption of its Artificial Intelligence Platform (AIP), which enables customers to deploy generative AI applications in the context of their businesses, for the improvement in deal activity. Given that the AI software market is predicted to exceed annual revenue of $1 trillion in 2032 compared to $170 billion last year, Palantir has a lot of room for growth in the long run.

What should investors do?

While it is true that Palantir’s rally has made the stock expensive, there is a good chance that it may be able to justify its rich valuation thanks to a combination of healthy top- and bottom-line growth. AI is not just hype for the company’s business and the new business that it has been winning should eventually lead to stronger earnings growth thanks to its improving margin profile.

So, if Palantir continues to retreat following the analyst downgrade, savvy investors can consider accumulating this AI stock for the long run as it seems on its way to becoming a top AI software play.

Should you invest $1,000 in Palantir Technologies right now?

Before you buy stock in Palantir Technologies, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Palantir Technologies wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

*Stock Advisor returns as of April 4, 2024

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Palantir Technologies. The Motley Fool has a disclosure policy.

Is Palantir Technologies Stock a Buy Now? was originally published by The Motley Fool

[ad_2]

Source link