Stock to Buy Hand Over Fist Before It Does")

Artificial intelligence (AI) might just be the hottest-ticket item in the stock market right now. Euphoria surrounding the technology sent the Nasdaq Composite soaring over 40% last year. Moreover, megacap tech enterprises such as the “Magnificent Seven” have contributed greatly to the S&P 500‘s new record highs.

Among the Magnificent Seven stocks, Microsoft and Nvidia often find themselves at the center of media coverage — and for good reason. Microsoft is a major investor in ChatGPT developer OpenAI. Meanwhile, demand for Nvidia’s graphics processing units (GPUs) is unprecedented as applications in quantum computing and machine learning skyrocket.

One company that I see as overlooked is e-commerce and cloud computing specialist Amazon (NASDAQ: AMZN). The company has made some interesting investments in AI. But slowing growth in its cloud segment coupled with a strained macroeconomy have some investors wary of the company’s prospects.

Let’s dig into why 2024 might be a good year for Amazon investors. More importantly, taking a thorough look at the company’s position in the AI landscape may shed some light on why Amazon should not be discounted relative to its peers.

The Nasdaq could be headed higher

The Nasdaq Composite index has been around for a little over 50 years. In that time frame, it has only produced negative annual returns 14 times.

Over the last two decades, however, the Nasdaq has only dropped by 30% or more on three occasions: 2002, 2008, and 2022. Keep in mind that 2008 was a difficult period in financial history, as it marked the beginning of the Great Recession. Additionally, 2022 was perhaps equally as debilitating for investors due to rampant inflation. But over the last couple of years, the Federal Reserve has swiftly taken action — increasing interest rates in an effort to curb rising inflation.

One thing that 2002 and 2008 share in common is that following steep declines, the Nasdaq rebounded sharply in consecutive years thereafter. Between 2003 and 2007, the Nasdaq returned an average of 16% per year. Furthermore, from 2009 to 2010 the index rose by an average of 30%.

While it’s important to understand that past results do not guarantee future performance, the analysis above highlights that the capital markets tend to operate with a level of resiliency. Given the impressive performance of the Nasdaq in 2023, coupled with rising interest in AI, this year could be another good one for the tech-heavy index.

Keep an eye on Amazon’s AI investments

Back in September, Amazon announced a multibillion-dollar investment in Anthropic, a competitor to OpenAI. The partnership with Anthropic contained many interesting features, the bulk of which are aimed at bolstering Amazon’s cloud business.

For the last couple of years, businesses of all sizes have scaled back on budgets and operated under much tighter financial controls. This dynamic greatly impacted tech businesses as demand for enterprise software waned. Amazon was not immune to this trend, and sales from its cloud business have slowed down. To add another layer of complexity, Amazon’s cloud unit represents nearly 70% of the company’s operating profits.

After looking at management’s commentary surrounding the Anthropic investment, it becomes more clear how Amazon plans to use this relationship to spark new interest in the cloud. Per the terms of the deal, Anthropic will be using Amazon Web Services (AWS) as its primary cloud provider. Moreover, Anthropic will also be using Amazon’s in-house semiconductor chips to train future generative AI models.

In a way, Anthropic could end up serving as a lucrative source of lead generation for AWS. As Amazon continues to introduce more AI-powered applications in the cloud, the company could very well begin to see an uptick in demand thanks to Anthropic.

I see the potential of the Anthropic relationship as largely underappreciated, if not misunderstood. Just as Microsoft is implementing ChatGPT across its operating system, Amazon could replicate this template in order to spur new acceleration in AWS.

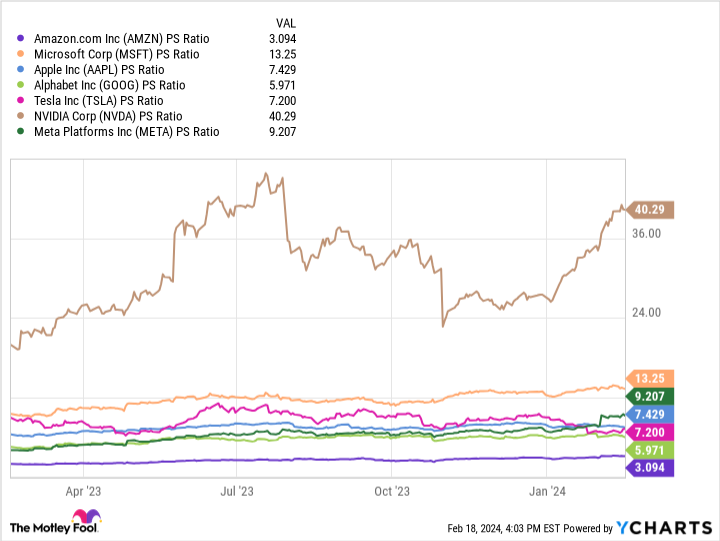

Amazon’s valuation looks appealing

The chart above shows Amazon benchmarked against the Magnificent Seven members on a price-to-sales (P/S) basis. At a P/S of 3.1, Amazon is the lowest-valued stock among this cohort based on this metric.

The primary reason I think Nvidia and Microsoft are trading at noticeable premiums is that both companies have already shown investors how AI is positively impacting their businesses. The trends above could suggest that investors think Amazon is lacking in AI capabilities relative to its peers, or the company simply isn’t showing enough growth to garner a premium valuation.

In either case, I see Amazon stock as dirt-cheap right now. AI has myriad applications and has the potential to disrupt Amazon’s core e-commerce and cloud businesses.

I think the company is taking the right steps to position itself for long-term sustained growth. While Amazon may be overshadowed by others in big tech, I do not think the company’s potential in the AI landscape should be discounted. Right now could be a unique opportunity to scoop up shares at an attractive valuation for long-term investors.

Should you invest $1,000 in Amazon right now?

Before you buy stock in Amazon, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Amazon wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

*Stock Advisor returns as of February 20, 2024

Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. Randi Zuckerberg, a former director of market development and spokeswoman for Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool’s board of directors. John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Adam Spatacco has positions in Alphabet, Amazon, Apple, Meta Platforms, Microsoft, Nvidia, and Tesla. The Motley Fool has positions in and recommends Alphabet, Amazon, Apple, Meta Platforms, Microsoft, Nvidia, and Tesla. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

History Says the Nasdaq Could Soar in 2024: 1 Artificial Intelligence (AI) Stock to Buy Hand Over Fist Before It Does was originally published by The Motley Fool

: Now Phenomenally Cheap with a 0.6x PEG Ratio")