One of the greatest aspects about putting your money to work on Wall Street is there are countless ways to grow your wealth. Regardless of your risk tolerance or investment focus, there are thousands of individual companies and/or exchange-traded funds (ETFs) that can meet your criteria.

But among this endless sea of possible investment strategies, one tends to rise above the pack. I’m talking about buying high-quality dividend stocks and hanging onto these positions over an extended timeline.

Recently, the analysts at Hartford Funds, in collaboration with Ned Davis Research, updated their data sets from an extensive study on dividend stocks that was released last year (“The Power of Dividends: Past, Present, and Future”). This duo compared the performance and volatility of dividend-paying stocks to non-payers over a half century (1973-2023).

Following the recent update, Hartford Funds found that non-paying public companies averaged a 4.27% annual return over the prior half-century, and were 18% more volatile than the benchmark S&P 500. By comparison, dividend payers delivered a 9.17% average annual return over the prior 50 years, and did so while being 6% less volatile than the S&P 500.

Companies that are regularly sharing a percentage of their profits with investors tend to be profitable on a recurring basis and are often able to provide transparent long-term growth outlooks. In short, these are businesses we’d expect to rise in value over time and make their patient shareholders richer.

But not all dividend stocks are created equally. Although some ultra-high-yield stocks — “ultra-high-yield” in the sense that their yields are at least four times higher than the S&P 500 — are more trouble than they’re worth, select high-octane income stocks can be true gems.

What follows are two beaten-down ultra-high-yield dividend stocks — with an average yield of 7.57% — that are historically cheap and ripe for the picking by opportunistic income seekers.

AT&T: 6.43% yield

The first supercharged dividend stock that’s exceptionally cheap and begging to be bought right now is telecom titan AT&T (NYSE: T). Though AT&T’s dividend has remained static at $0.2775 per quarter, its yield is a safe and hearty 6.4%!

But in spite of this phenomenal payout, AT&T’s stock has fallen by 42% since late 2019.

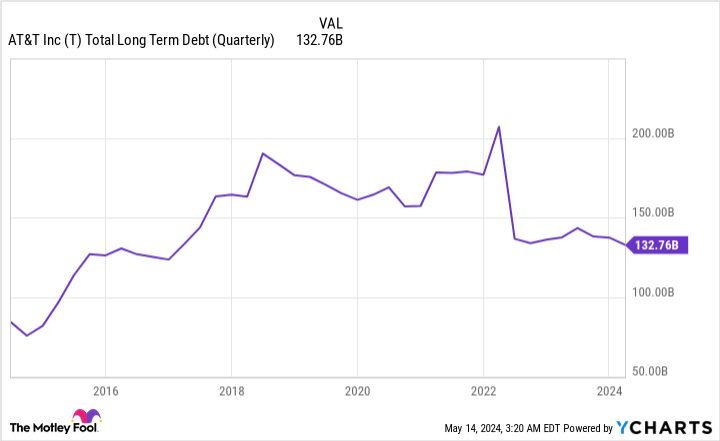

One of the reasons for this weakness is rising interest rates. The company closed out the March quarter with $132.8 billion in total debt. Lugging around a sizable amount of debt is pretty common for legacy telecom companies. Unfortunately, with the Fed aggressively raising rates to combat historically high inflation, any future refinance activity and/or deal-making could be notably costlier to AT&T.

The other concern for AT&T has to do with a story from The Wall Street Journal released in July 2023. The WSJ report alleges that legacy telecom companies could face hefty cleanup and environmental/health-related costs tied to their use of lead-sheathed cables. With so much debt already on their balance sheets, the last thing telecom companies need is a potential multibillion-dollar liability.

While these are tangible headwinds that current and prospective AT&T investors shouldn’t sweep under the rug, it’s important to recognize that neither are as concerning as the company’s beaten-down share price would suggest.

Although AT&T’s $132.8 billion in total debt is daunting, the company’s financial situation has dramatically improved over the last two years. When AT&T divested WarnerMedia in April 2022, and it subsequently merged with Discovery to create a new media entity, Warner Bros. Discovery, AT&T enjoyed more than $40 billion in concessions — e.g., Warner Bros. Discovery taking on select lots of debt previously held by AT&T. Over the last two years (ended March 31, 2024), the company’s net debt has declined from $169 billion to $128.7 billion.

As for the WSJ report, AT&T has directly refuted claims that its lead-clad cables present a health hazard. Further, liability claims are typically handled in the U.S. court system. If AT&T were to ever face cleanup or liability costs associated with these lead-sheathed cables, it would take years for the court to come to a verdict. Over that time, its balance sheet would likely improve.

Aside from a firmer balance sheet, AT&T’s core operations continue to benefit from the 5G revolution. Wireless service revenue is on pace to increase by 3% in 2024, with churn rates remaining near a record low.

Meanwhile, AT&T’s broadband segment got off to another strong start in the new year with the net addition of 252,000 AT&T Fiber subscribers. The company has added at least 1 million net broadband customers for six consecutive years.

Though AT&T’s operating model isn’t flashy, and its growth heyday ended decades ago, it’s capable of delivering mid-single-digit sales and earnings growth, along with predictable operating cash flow. Valued at just 7.5 times consensus earnings per share (EPS) in 2025, AT&T is an undeniable bargain.

Altria Group: 8.7% yield

The second beaten-down ultra-high-yield dividend stock that’s historically cheap and begging to be bought right now is tobacco giant Altria Group (NYSE: MO). Altria has raised its payout 58 times over the past 54 years, which places it in elite company among a handful of other “Dividend Kings.”

The clear-cut challenge for tobacco stocks is that consumers have become more informed about the potential long-term health hazards of using tobacco products. In the U.S., which is Altria’s domain, the percentage of adults who smoke cigarettes has declined from around 42% in the mid-1960s to just 11.5%, as of 2021. A steadily shrinking pool of patients is a worrisome situation for any company.

Additionally, Altria’s high-growth days are now well in the rearview mirror. With interest rates held near historic lows for much of the decade prior to 2022, investors flocked to faster-growing companies. This meant mature businesses like Altria slowly became the stock market’s equivalent of chopped liver. Not surprisingly, shares have fallen by 42% since peaking in 2017.

While sin stocks like Altria Group aren’t going to be every investor’s cup of tea, it’s nevertheless a company that possesses catalysts that can still deliver rock-solid returns to patient investors.

One factor that continues to benefit Altria is its pricing power. Because nicotine is an addictive chemical, the company often has little trouble passing along price hikes that can partially or fully offset any decline in cigarette shipments.

To add to the above, it certainly doesn’t hurt that Altria is a market share juggernaut in the United States. The company’s premium Marlboro brand accounted for a 42% share of the U.S. cigarette market in the first quarter, while its other premium and discount brands tacked on another 4.4% in collective market share. Controlling nearly half of U.S. cigarette market share makes it even easier for Altria to raise prices on its customers.

However, Altria’s game plan involves more than just price hikes. Management aims to introduce new sales channels that can reignite the company’s growth engine.

For instance, Altria acquired electronic-vapor company NJOY Holdings in June 2023 for $2.75 billion. While Altria’s sizable investment in e-vape company Juul didn’t pan out, buying NJOY was a no-brainer thanks to a clear-cut differentiating factor.

At the time the buyout was completed, NJOY had received a half-dozen marketing granted orders (MGOs) from the U.S. Food and Drug Administration (FDA). These MGOs are effectively permission slips from the FDA that allow e-vape products to remain on retail shelves. The overwhelming majority of e-vapor products lack MGOs, and could therefore be pulled at any moment.

Furthermore, Altria is a longtime equity stakeholder in Canadian marijuana licensed producer Cronos Group. Recently, the U.S. federal government announced that cannabis would soon be rescheduled to a less-stringent classification of a controlled substance. This may open the door for Canadian medical marijuana producers to enter the U.S. market.

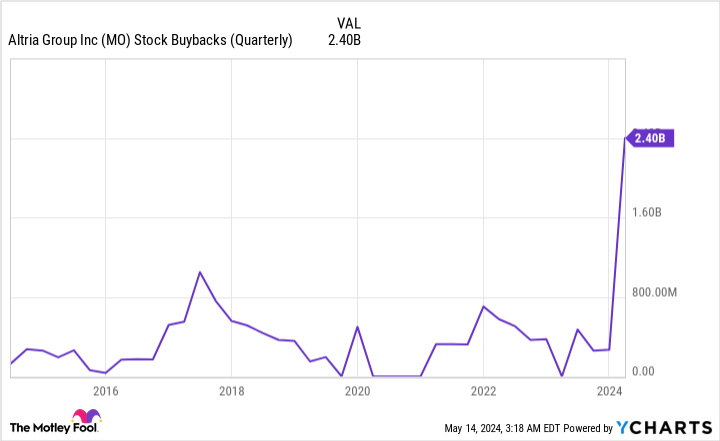

Lastly, Altria Group has a stellar capital-return program. The company’s board authorized a $2.4 billion accelerated share repurchase program, and plans to complete an additional $1 billion in buybacks before the end of this year.

A forward price-to-earnings ratio of 8.5, coupled with a yield of 8.7%, is highly attractive for income seekers.

Should you invest $1,000 in AT&T right now?

Before you buy stock in AT&T, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and AT&T wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005… if you invested $1,000 at the time of our recommendation, you’d have $559,743!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of May 13, 2024

Sean Williams has positions in AT&T and Warner Bros. Discovery. The Motley Fool has positions in and recommends Warner Bros. Discovery. The Motley Fool has a disclosure policy.

Time to Pounce: 2 Beaten-Down Ultra-High-Yield Dividend Stocks That Are Historically Cheap and Begging to Be Bought Right Now was originally published by The Motley Fool

: Now Phenomenally Cheap with a 0.6x PEG Ratio")